Dubai Residential Real Estate Market Forecast to 2040

Future Price Trends

Residential real estate prices in Dubai have seen strong increases recently, driven by high demand from both local and international buyers. There was a year-on-year increase of about 20% in home prices during the third quarter of 2024, and the average sales price in 2024 rose by about 20% to approximately 1,597 AED per square foot. These significant increases came after a period of moderate growth between 2018 and 2020, confirming the return of momentum to the Dubai real estate market after the COVID-19 pandemic.

Prices are expected to continue their upward trajectory in the medium term, but at a more stable pace. Knight Frank estimates an additional rise of about 8% in 2025, and local real estate developers expect annual price increases of between 5-8% in the coming few years. These forecasts are based on strong and sustainable demand but also consider an increase in supply and a better market balance. Over the long term up to 2040, prices are likely to continue rising supported by population growth and planned major projects, although there may be short-term correction cycles. For example, villa prices currently exceed the previous peak levels (in 2014) by more than 30%, which means the market may experience a relative slowdown or minor correction after periods of significant increase before continuing its sustainable upward trend.

Supply and Demand

The supply and demand real estate market in Dubai is moving towards a balanced growth supported by Dubai's Vision 2040 and upcoming urban development plans. The population has risen from about 3.4 million in 2020 to 3.68 million currently (2025), and according to Dubai's Vision 2040, the population is targeted to reach between 5.8 and 7.8 million by 2040. This rapid population growth will lead to a significant increase in demand for residential units over the next two decades. Indeed, demand for residential properties has maintained its momentum, driven by the influx of new residents and investors, especially the wealthy looking for luxury homes or investment returns. Policies such as visa regulations (such as the Golden Visa) and social stability have made Dubai an attractive destination for those wishing to settle and work, which enhances the demand for housing sustainably.

In contrast, the property supply is responding at an accelerated but cautious pace to avoid market saturation. The average annual delivery of new residential units was about 32,000 units in 2021, which increased to 37,000 units in 2023. However, considering the targeted population increase, it may be necessary to deliver between 37,600 and 87,700 residential units annually until 2040 to meet the demand. Market reports indicate that about 300,000 additional residential units are expected to be delivered by 2029 – 80% of which are apartments and 17% villas – but this level of supply may not be sufficient if population growth accelerates. In fact, experts warn that if the historical delays in project completion continue, only 210,000 units may be delivered in the next six years (until 2030), potentially creating a long-term housing shortage.

In terms of demand composition, there is an increasing preference for villas and townhouses compared to traditional apartments, as families prefer larger spaces post-pandemic. Demand is concentrated in key areas such as Downtown, Dubai Marina, Dubai South, and waterfront areas where amenities and modern lifestyles are available. This demand distribution indicates the importance of developing quality projects in these areas and directing investment towards real estate products that meet the needs of the middle and above-average segments of the population. In general, the supply and demand equation is expected to remain relatively balanced due to coordination between developers and the government within a unified vision, aiming to regulate the pace of new projects to prevent excess supply and maintain long-term price stability.

Return on Investment (ROI) and Comparison with Other Markets

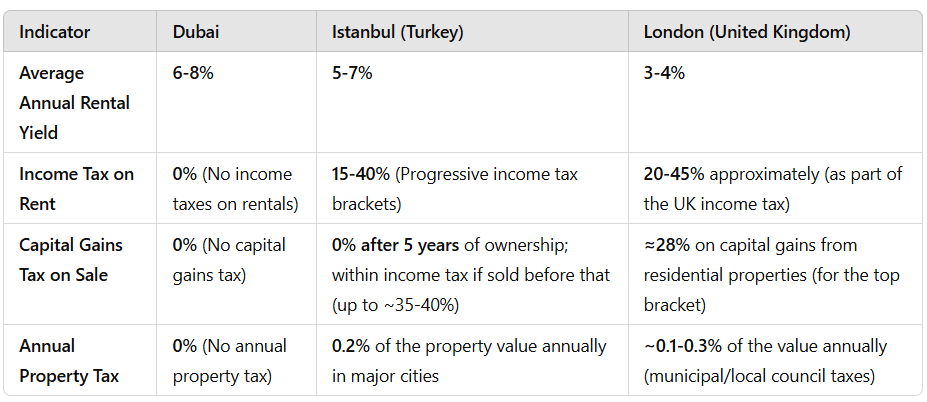

Dubai offers a return on investment in residential properties that is among the highest globally, supported by high rental rates and the absence of property taxes. The average gross rental yield in Dubai is about 6-8% annually for residential properties, a rate that outperforms most major global cities. In comparison, Istanbul in Turkey achieves rental yields of around 5-7% annually on average for residential properties, while returns in cities like London are much lower (about 3-4%) due to high property values and low rental rates.

As is evident, net returns in Dubai are significantly higher due to tax exemptions and relatively high rents. For example, an investor in Dubai retains almost all rental income without tax deductions, while rental income in Turkey is subject to a progressive tax that may reach 35-40% of the profit (with certain exemptions for residential properties). In markets like the UK, not only is there a high income tax on rents, but there are also high transaction taxes (such as stamp duty in London, which can be a significant percentage of the property price, in addition to about 28% capital gains tax on the sale). In contrast, the investor in Dubai enjoys a low-cost environment (except for a one-time property transfer fee of 4%), which raises the true net return.

In addition to rental yield, Dubai has also achieved significant capital appreciation in recent years, enhancing the total return on investment. An investor who purchased a property two or three years ago may have realized a 20-30% growth in asset value in addition to annual rental income. In contrast, Turkey has also seen significant nominal property price increases driven by inflation (exceeding 50% annually in Turkish lira at times), but sharp fluctuations in the lira's value and high inflation have reduced the real return when evaluated in dollars or hard currencies. Meanwhile, mature markets like London and New York, despite their relative stability, have experienced much lower price growth (often less than 5% annually) due to market maturity and high price bases, in addition to tax costs that reduce the net return for investors.

On the attractiveness of international investment, Dubai holds a prestigious position among global real estate destinations due to the ease of foreign ownership (freehold system) and competitive business environment. Investors are attracted to Dubai for the tax-exempt profits and streamlined regulatory procedures in addition to the promise of high rental returns. Additionally, the cost of entering the Dubai market (property prices relative to quality and location) remains lower than its counterparts in major global cities, making high-quality assets with good returns accessible for relatively less capital. This unique combination of high returns and relatively low risks (due to economic stability and a good regulatory environment) makes Dubai a strong competitor to investment destinations like Istanbul, which lacks currency stability, or Western cities that burden investors with taxes.

The following table provides a comparison between Dubai and some competing markets in aspects of return and investment costs:

Impact of Economic Factors (Inflation, Interest Rates, and Stability)

Dubai enjoys a stable and diversified economy, although its real estate market, like others, is affected by macroeconomic variables locally and globally. Inflation rates in the UAE are low and controlled compared to other emerging markets; inflation was about 1.6% in 2023 and is expected by the central bank to reach about 2.3% in 2024 and 2025, driven by moderate increases in rents and living costs. This moderate inflation is positive for the real estate sector, as it maintains spending and investment power without significant erosion of purchasing power, unlike markets suffering from high inflation that pressures household incomes and increases construction costs. Additionally, the UAE dirham's peg to the US dollar provides monetary stability and shields the country from exchange rate fluctuations, meaning real estate investors in Dubai do not face the risks of currency depreciation that may occur in other countries (such as the significant fluctuations of the Turkish lira).

Regarding interest rates, there was a global increase in 2022-2023 as monetary policy tightened, led by the US Federal Reserve, and since the dirham is pegged to the dollar, this led to an increase in interest rates in the UAE to a level of 5.4% (the base rate at the Central Bank of the UAE since July 2023). The rise in interest rates has increased the cost of real estate financing (mortgages) compared to historically low levels, which may limit some buyers' ability to borrow and thus cool demand slightly, especially among end-users. However, it has been noted that a significant portion of Dubai's real estate transactions are cash purchases or financed minimally by financially robust buyers, which has mitigated the impact of rising interest on the market as a whole. The International Monetary Fund has highlighted the robustness of the UAE banking system and its reduced exposure to the real estate sector to about 19.6% of total loans (as of September 2024), indicating no dangerous credit bubbles. In the foreseeable future, economic experts expect a global reduction in interest rates starting from 2025 as global inflation declines, which could give an additional boost to Dubai's real estate market by reducing financing costs and increasing the appetite for borrowing-based purchases.

Economic stability is one of the key factors attracting people to Dubai. The emirate enjoys strong and balanced economic growth – with the real GDP of the UAE expected to grow by about 3.9% in 2024 and 6.2% in 2025, driven by non-oil sectors growing at ~5.4% – which means new job creation and continued population influx. Sectors such as trade, tourism, and transport are performing excellently (Dubai recorded a record non-oil trade exceeding 2.4 trillion AED in 2023, and tourist numbers grew by 11% in the first quarter of 2024). This economic momentum enhances confidence and increases demand for real estate for both residential and investment purposes. Additionally, the Dubai government is keen on maintaining stability in the real estate market through prudent policies (such as regulating speculative activities through relatively high registration fees, and setting regulations to protect investors and tenants).

Despite strong fundamentals, there are external economic factors that could affect Dubai's real estate market up to 2040. The most significant potential risk is a global economic slowdown or a global recession; if global growth significantly declines, the movement of investors and residents to Dubai may slow down, reducing real estate demand below expectations. Also, oil prices, although Dubai has reduced its direct dependence on oil revenues, any sharp and sustained drop in oil prices could impact government spending in the region as a whole and weaken investment appetite. Finally, regional competition from other Gulf cities (such as Riyadh or Doha) that are heavily investing in attracting businesses and residents could pose a challenge, although Dubai currently holds a leading position thanks to its established infrastructure and global openness. Overall, the economic outlook for Dubai remains positive and stable, with a high ability to adapt to changes, meaning the residential real estate market will benefit from this stability over the coming decades, with periodic monitoring for any global economic developments.

Impact of Dubai's Urban Plan 2040 on the Real Estate Sector

Dubai's Urban Vision 2040 forms a comprehensive roadmap for the future of urban development in the emirate, and it has a direct impact on the residential real estate sector in terms of the distribution of projects and promising areas for growth. The plan aims to transform Dubai into a sustainable city with distributed growth by creating and developing five main urban centers specialized in different orientations, ensuring a balanced distribution of population and economic activities across the city and reducing pressure on the traditional city center. These centers include areas with different orientations: a historical cultural center (such as Deira and Bur Dubai for heritage preservation), a financial and commercial center (Downtown Dubai, Business Bay, and DIFC), a tourist and coastal center (Dubai Marina, Palm Jumeirah, and other beach areas), in addition to emerging centers in South Dubai and around the Expo site. Directing growth through these five centers will lead to a broader spread of new residential projects and provide investors with options in multiple areas instead of concentrating all development in limited spots.

The plan clearly focuses on improving the quality of life and the sustainable aspect of the city, which enhances Dubai's residential appeal. By 2040, Dubai aims for 60% of its area to be green and natural spaces, meaning the creation of more parks, recreational areas, and open spaces within urban projects. This will make residential complexes more attractive to residents seeking a healthy and family-friendly environment, and increase the value of properties near parks and waterfronts. Additionally, public transportation networks will be significantly expanded – including the Dubai Metro – so that most residents can reach a public transport station on foot (targeting that most residents will be within 800 meters of a metro or bus station by 2040). This infrastructure development will create new hot real estate areas around metro stations (Transit-Oriented Developments), where property values will rise due to their proximity to transportation and easy connectivity to the rest of the city.

Another fundamental aspect of Vision 2040 is the massive expansion of the waterfront in the emirate. The vision includes giant projects to increase the length of beachfronts by 400% compared to the current situation. For example, new islands and coastal areas will be developed, such as the Dubai Islands project, which adds 50 kilometers of waterfront and 23 kilometers of beaches, in addition to the Palm Jebel Ali project, which will add 110 kilometers of coastal fronts and 81 kilometers of new beaches, providing housing for about 38,000 families. These coastal projects will accommodate the construction of dozens of luxury resorts and hotels (85 five-star hotels in Palm Jebel Ali alone) along with thousands of new residential units with sea views. Thus, the real estate sector will witness the launch of new upscale beachfront residential communities, meeting investors' appetite for waterfront properties and increasing the supply in the luxury housing and tourism sector.

Additionally, Dubai's Vision 2040 addresses providing suitable housing for all segments of society amidst the expected population growth. The plan includes encouraging developers to build affordable housing through incentives and facilitations, ensuring the availability of homes for the middle-income group, who will form a large part of Dubai's new residents. Policies also tend toward modernizing planning regulations to allow the development of multi-use projects and smart residential communities that employ innovative planning solutions to efficiently accommodate more residents in existing urban areas without compromising the quality of life. Experts anticipate that public-private partnerships will play a pivotal role in implementing this vision, whether through infrastructure development or major real estate projects, to ensure the achievement of the plan's goals.

As a result, the impact of Vision 2040 will be highly positive on the real estate market; on one hand, it will create new development areas and wide investment opportunities (coastal and urban), and on the other hand, it will make the supply growth thoughtful and aligned with the expected demand growth, avoiding sharp surplus cycles. With the implementation of the plan, by 2040 Dubai will become a more balanced, widespread, and harmoniously urbanized city – enhancing its attractiveness for living, working, and investing alike, and supporting property values in the long term due to the quality of life and world-class infrastructure.

Impact of the Tax-Free Environment on Dubai's Attractiveness

The near-total tax exemption in Dubai is one of the most important factors supporting the attractiveness of the real estate market for both local and international investors. The Dubai government does not impose any personal income taxes on residents, there is no corporate profit tax in the residential real estate sector, and no annual property taxes on properties (unlike most cities in the world). Additionally, there is no capital gains tax when selling a property, meaning that any increase in property value upon resale is considered a complete profit for the investor. This unique tax policy means that all rental and sale profits remain entirely with the investor, which is rare globally.

For comparison, in many other markets, an investor faces several types of taxes: for example, in Turkey, there is an income tax on rentals that can reach 35% or more depending on the income bracket, and there is also an annual property tax (about 0.2% of the property value in Istanbul), in addition to a tax on profits if sold within less than 5 years of purchase. In Western countries, the tax burden is higher; for instance, in Britain, there is an annual tax (council tax) and municipal fees, and income tax on rentals according to the bracket could reach about 40%, and a 28% capital gains tax on the sale of investment property, not to mention high stamp duties at purchase. Such burdens significantly reduce the net return for the investor and the profitability of real estate investment in those countries.

Thus, Dubai offers an exceptional competitive advantage through its absence of taxes, significantly enhancing real estate investment returns. For example, an investor in Dubai who achieves a 7% annual rental yield retains this entire yield , whereas their counterpart in another market with a similar yield might lose a third or half of it to taxes. Additionally, the absence of property taxes in Dubai also reduces the cost of owning property over the long term; an investor does not have to pay an annual tax to keep their property, encouraging them to adopt a long-term investment perspective without ongoing costs.

This tax situation has made Dubai a preferred destination for investors seeking tax-safe havens for their properties. In recent years, Dubai has seen notable capital inflows from Europe, Asia, and North America, much of which is due to investors' desire to diversify their portfolios in a tax-exempt market and benefit from asset value growth without tax restrictions. International reports have indicated that the UAE (and specifically Dubai) attracted large numbers of wealthy individuals in 2022 and 2023 as a destination for residence and investment, benefiting from world-class infrastructure and a luxurious lifestyle in addition to tax incentives.

It is worth noting that Dubai only imposes limited fees during real estate transactions – the most significant being property transfer fees of 4% paid once at the time of sale registration at the Land Department . These fees are moderate compared to taxes in other countries, and they are often negotiated as part of the deal price. Beyond that, an investor might only face service and maintenance fees imposed by the developer or the owners' association to maintain the property, which are operational costs and not government taxes.

In conclusion, the absence of taxes in Dubai not only enhances the financial return for the investor but also adds a high degree of certainty to economic feasibility calculations. Investors can calculate their future returns confidently without fearing tax policy changes that could deduct from their profit. This transparency and stability in the tax environment, along with other factors such as the ease of money transfers and 100% foreign ownership in free zones and freehold areas, make Dubai one of the best real estate investment environments globally. It has been reflected in the fact that a large proportion of property purchases in Dubai are made by international investors seeking a safe haven for their funds. With these investor-supportive policies continuing, Dubai is expected to remain at the forefront of destinations attracting real estate capital until 2040 and beyond.

Related Articles

Dominica Taxes Explained: A Complete Guide for Citizenship by Investment Applicants

Many prospective applicants ask whether acquiring a Dominica passport means they will have to pay income tax, wealth tax, or taxes on their global assets.

The short answer is no.

However, understanding the difference between citizenship and tax residency is essential before making any investment decision.

This guide explains everything you need to know about the tax system in the Commonwealth of Dominica, including personal income tax, corporate taxation, capital gains, inheritance, VAT, and how taxes apply to Citizenship by Investment (CBI) applicants.

Dubai Real Estate Outlook After Recent Events: Are We Entering a Smarter Opportunity Phase?

Recent regional developments have raised important questions among investors and buyers alike:

What’s next for Dubai’s real estate market? And is this the right time to invest?

Following the announcement of a ceasefire, market sentiment has begun to stabilize. However, understanding the real impact on Dubai real estate requires a deeper look at economic fundamentals, investor psychology, and market dynamics.

In this article, we provide a realistic, data-driven perspective on what to expect in the coming months.

Dominica Citizenship by Investment Program

Obtaining a second citizenship has become a strategic decision for global investors, entrepreneurs, and families seeking mobility, financial security, and international opportunities. One of the most attractive and affordable options available today is the Dominica Citizenship by Investment Program (CBI).

Established in 1993, Dominica’s program is one of the most reputable and longest-running citizenship by investment programs in the world. It offers investors and their families the opportunity to obtain a second passport in as little as 4–6 months, with access to more than 150 countries visa-free.

This guide explains everything you need to know about the Dominica citizenship program, including investment options, eligibility requirements, benefits, required documents, and the application process.

Comments (0)

You need to be logged in to comment